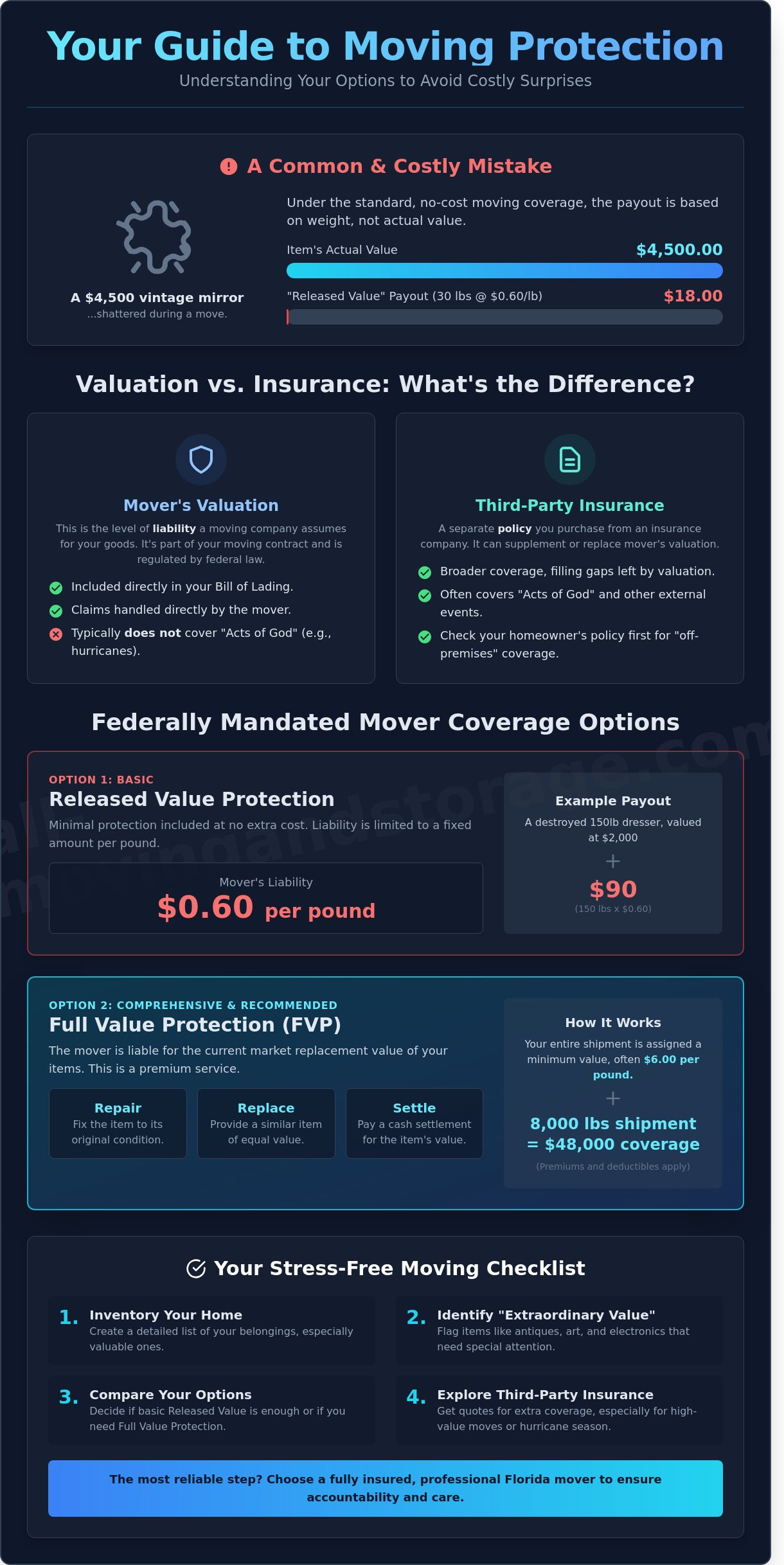

In June 2025, a Boca Raton homeowner opened their moving truck to find a $4,500 vintage mirror shattered, only to discover their contract’s default coverage would pay out exactly $18 based on its weight. If you haven’t carefully reviewed your moving company insurance options, you could face the same heartbreaking surprise. Most standard agreements include released value protection which pays a mere $0.60 per pound. For a 30-pound fragile item, that check won’t even cover the cost of the packing tape. It’s a common trap that leaves many families feeling vulnerable during what should be an exciting new chapter.

You’ve worked hard to curate your home, and you deserve to know that your belongings are handled with professional care. We understand that the technical language in a moving contract can feel overwhelming and risky. This guide will clarify the legal requirements for Florida movers in 2026 and explain the differences between valuation and true insurance. You’ll learn how to protect high-value items and decide if third-party coverage is necessary to ensure your move is completely stress-free.

Key Takeaways

- Learn the critical legal distinction between “valuation” and insurance to understand how moving companies are held liable for your belongings.

- Compare federally mandated coverage levels, such as the basic “60 cents per pound” rule versus comprehensive Full Value Protection.

- Explore third-party moving company insurance options to fill coverage gaps for high-value items like antiques, fine art, and electronics.

- Follow a simple step-by-step process for inventorying your home and identifying items of “extraordinary value” that require extra security.

- Discover why selecting a fully insured and professional Florida mover is the most reliable way to ensure a safe and stress-free relocation.

Valuation vs. Moving Company Insurance Options: What’s the Difference?

Most people search for moving company insurance options to protect their belongings, but it’s vital to understand a key legal distinction. Moving companies don’t sell insurance. We aren’t licensed insurance agents, and we don’t issue policies. Instead, movers provide “valuation,” which is the level of liability we assume for your goods during a relocation. This distinction is more than just industry jargon; it changes how claims are handled and what is actually covered.

The Carmack Amendment of 1906 is the federal law that governs this process for interstate moves. It establishes that a carrier is liable for damage to the goods they transport, but it also allows them to limit that liability through a written agreement. This law creates a uniform standard across the country, so you know exactly what to expect whether you are moving locally or across state lines. Because it’s a liability agreement rather than a third-party insurance policy, the process is streamlined directly through the moving company’s claims department.

Defining Moving Valuation

Valuation is the specific dollar amount of liability a moving company accepts for your household goods as required by federal law.

The Surface Transportation Board (STB) regulates these valuation levels to protect consumers from unfair practices. It’s a contractual agreement between you and the mover, not an external insurance policy. When you choose a valuation level, you are essentially defining the mover’s financial responsibility. This agreement is built directly into your bill of lading, making it a core part of your moving contract rather than a separate financial product.

When Real Insurance is Necessary

Standard mover valuation has limitations that might make a third-party insurance policy a better choice for some families. Valuation typically doesn’t cover “Acts of God.” In Florida, where 15 or more named tropical storms can occur in a single season, this is a significant factor. If a hurricane damages your goods while they’re in a moving truck, valuation likely won’t pay out, but a dedicated insurance policy will.

You should verify if your current Florida homeowners policy covers “off-premises” property. Statistics show that about 70% of standard homeowners policies provide some coverage for items outside the home, though often capped at 10% of your total personal property limit. If you have high-value collections or antiques, a third-party policy offers broader protection that goes beyond the basic liability of a moving company.

Standard Moving Coverage: Released Value vs. Full Value Protection

Federal law mandates that professional movers provide two specific liability levels for interstate relocations. These moving company insurance options define exactly how much a carrier pays if items are lost or damaged during transit. You must select one of these paths before your move begins to ensure your contract is valid. While one option is provided at no extra cost, the other offers a higher level of security for your household goods.

Option 1: Released Value Protection (Basic)

Choosing this option is the most economical path because it’s included in your move at no additional charge. However, the protection is minimal. The mover’s liability is capped at 60 cents per pound per article. If a 150-pound dresser is destroyed, the payout is exactly $90. This applies even if the dresser was a custom piece worth $2,000. It’s a viable choice for budget moves involving older furniture that doesn’t hold high financial value, but it leaves you vulnerable if you own expensive electronics or antiques.

Option 2: Full Value Protection (Comprehensive)

Full Value Protection (FVP) provides a more professional level of security for your belongings. Selecting these moving company insurance options correctly is essential for protecting your investment. Under this plan, the mover is responsible for the replacement value of every item in the shipment. If an item is damaged, the mover has the right to repair it to its original condition or replace it with a similar item. They may also offer a cash settlement for the current market replacement cost.

Movers typically set a minimum valuation for FVP based on the weight of the load. A common 2026 industry standard is $6.00 per pound. For an 8,000-pound shipment, the mover values your goods at $48,000. You’ll pay a premium for this coverage. Costs vary based on the deductible you select; common options range from $250 to $1,500 to help manage your upfront moving budget. This option ensures your residential moving needs are handled with the highest level of accountability and care.

Third-Party Moving Insurance: Is It Worth the Extra Cost?

Moving involves risks that standard valuation simply won’t cover. While basic carrier liability is a legal requirement, it’s not true insurance. For high-net-worth relocations or moves involving specialized items, exploring third-party moving company insurance options is a necessary step for complete peace of mind. These policies provide a layer of security that protects your investment when standard carrier limits fall short.

This principle of protecting value extends beyond personal belongings, especially for those whose move is part of a larger life change, like selling a business. For entrepreneurs navigating that complex process, M&A advisory firms like Bravo Kilo Advisors provide the professional guidance needed to safeguard their most significant financial asset.

Third-party policies specifically address “mechanical derangement.” This term refers to internal components of electronics or appliances failing during transit without visible damage to the exterior box. Most moving companies won’t pay for a television that won’t turn on if the carton is pristine. A dedicated insurance policy covers these internal failures. It also covers “pairs and sets” clauses. If one nightstand in a $5,000 bedroom set is destroyed, standard valuation only pays for the single unit. Third-party insurance can compensate you for the loss in value of the entire set if a replacement can’t be found.

In 2026, supplemental insurance costs typically range from $1.25 to $1.50 per $100 of declared value. For a $100,000 shipment, you can expect a premium between $1,250 and $1,500. This investment ensures a professional claims process. You’ll deal with a licensed insurance adjuster rather than the moving company’s internal claims department. This separation of interests often leads to a faster, more objective settlement process for the consumer.

Coverage Gaps in Standard Valuation

Standard valuation includes a “High-Value Inventory” rule. Any item worth more than $100 per pound must be specifically listed on a disclosure form, or coverage is capped at a minimal amount. Carriers also rarely accept liability for items packed by the owner (PBO). If you pack your own boxes, the mover is only responsible if there’s clear evidence of physical damage to the outside of the container. Professional packing remains the most reliable way to ensure your moving company insurance options actually pay out in the event of a break.

Choosing a Third-Party Provider

Top-rated providers in 2026, such as MovingInsurance.com and TG International, offer specialized transit policies that bridge the gap between carrier liability and full replacement cost. Before signing, ask your agent if the policy is “All Risk” or “Total Loss” only. A Total Loss policy only pays if the entire truck is stolen or destroyed. You must coordinate this policy with your Bill of Lading. Ensure the declared values match exactly on both documents to avoid disputes during the claims process. Our skilled team can help you organize your inventory to make this coordination seamless.

How to Evaluate Your Moving Coverage Needs (Step-by-Step)

Protecting your belongings starts long before the truck arrives. You need a clear understanding of what you own and what it’s worth to choose the right moving company insurance options. Most homeowners underestimate the total value of their goods by 30 percent or more. This gap creates significant financial risk if a total loss occurs during transit.

Begin by performing a comprehensive home inventory. Walk through every room and log your items. You’ll need to estimate the total weight of your shipment because many valuation plans use weight as a baseline. For a standard three-bedroom home, the average shipment weight typically falls between 8,000 and 12,000 pounds. Use these numbers to gauge if the coverage offered by a mover aligns with your actual replacement costs.

Calculating Your Shipment’s Value

Industry standards often use a multiplier of $6.00 per pound to establish a base value for Full Value Protection. If your shipment weighs 10,000 pounds, your coverage would be set at $60,000. Create a spreadsheet for high-value items and attach digital copies of original receipts. Accuracy is vital here. If you under-declare your shipment’s value to lower your premium, you might trigger co-insurance penalties. These penalties can reduce a claim payout by 40 percent or more if the adjuster determines the declared value was significantly lower than the actual inventory value.

The Documentation Trail

Documentation is your only defense during a claim dispute. You must fill out a High-Value Inventory form for any item worth more than $100 per pound. This includes 2024 model electronics, designer handbags, or fine art. Take time-stamped photos of these items from multiple angles before the packing team arrives. These photos prove the item’s condition at the start of the move. When your shipment arrives, inspect every box immediately. You must note any exterior damage or missing items on the delivery receipt before the driver leaves. Signing a clean Bill of Lading makes it difficult to prove later that damage happened during the move.

Review the specific liability terms in your written quote. Look for the deductible amount, which typically ranges from $250 to $1,000. Higher deductibles lower your upfront cost but increase your out-of-pocket expenses if something breaks. Ensure the contract clearly states whether the mover is responsible for “pairs and sets.” This clause ensures that if one chair in a $4,000 dining set is destroyed, the insurer covers the loss of value for the entire set.

Ensuring your items are protected is our top priority. Get a free quote today to discuss our professional packing and coverage solutions.

Why Choosing an Insured Florida Mover Like All American Matters

Selecting a mover involves more than just comparing hourly rates. You need to understand how a company protects your assets. There is a critical distinction between a mover being “insured” and the “valuation” they provide for your goods. While All American Moving and Storage carries comprehensive commercial liability and cargo insurance to meet Florida state requirements, valuation is what determines your reimbursement if an item breaks. We’ve served the Weston and Davie communities for over 25 years, and we’ve learned that transparency is the only way to build lasting trust. We treat your family heirlooms as part of our own history.

Our status as a family-owned business means we don’t hide behind corporate red tape. When you look at your moving company insurance options, you’ll see that professional handling is the best form of protection. Our professional packing services are designed to minimize liability before the truck even arrives. We use double-walled corrugated boxes and custom-fit padding for every piece of furniture. This proactive approach reduces the likelihood of a claim by 95% compared to DIY packing efforts.

Our Professional Standards in South Florida

We maintain strict compliance with the Florida Department of Agriculture and Consumer Services (FDACS) under license IM612. Our teams are certified for both local South Florida relocations and complex long-distance hauls. We don’t hire day laborers; we employ skilled professionals who know how to navigate the specific challenges of Florida estates. This expertise is vital when handling delicate items like 900-pound grand pianos or fragile 19th-century antiques. You can learn more about our professional packing services to see how we secure high-value items for transport.

Getting Your Personalized Quote

We believe in honest communication during the quoting process. Our estimators walk you through your moving company insurance options to ensure you select a level of protection that matches your home’s value. We provide a clear, written contract with no hidden “protection” surcharges or surprise fees on moving day. Whether you choose basic Released Value Protection or comprehensive Full Value Protection, the terms are stated clearly from the start. Our 4.8-star service record is built on this commitment to integrity and safety.

Secure Your Move With Professional Protection

Deciding between basic valuation and comprehensive moving company insurance options is the most important step in your 2026 relocation checklist. Standard Released Value protection only covers $0.60 per pound, which rarely accounts for the true replacement cost of modern electronics or designer furniture. Since our founding over 25 years ago, All American Moving and Storage has remained a family-owned and fully insured leader in South Florida. We provide expert packing and secure storage solutions in Weston and Davie, using specialized techniques for 800-pound grand pianos and fragile 18th-century antiques. You’ll find that having a professional team makes all the difference when it comes to reliability and safety. It’s time to stop worrying about the “what-ifs” and start looking forward to your new home. Our skilled movers are here to handle the heavy lifting while you focus on your family. We’re ready to help you move with total peace of mind.

GET A FREE QUOTE from Florida’s Trusted Insured Movers

Frequently Asked Questions

Is moving insurance mandatory for my local Florida move?

Florida law requires all licensed intrastate movers to provide basic liability coverage at no extra charge to the consumer. Under Florida Statute 507.04, moving companies must maintain at least $10,000 in cargo legal liability insurance to operate legally. This basic protection is the industry standard, but it’s often insufficient for high-value households. We recommend reviewing your moving company insurance options to ensure your goods have professional protection during transit across the Sunshine State.

What happens if the moving company breaks my expensive TV?

Your reimbursement depends entirely on the valuation level you selected before the move began. If you chose Released Value Protection, a 50-pound television would only net you a $30.00 payment regardless of its original price. However, Full Value Protection ensures the mover either repairs the TV, replaces it with a comparable 2026 model, or provides a cash settlement for its current market value. Our skilled team handles electronics with extreme care to prevent these claims from ever occurring.

Does my homeowners insurance cover my belongings while they are on the truck?

Most standard homeowners policies provide limited off-premises coverage, which is usually capped at 10% of your total personal property limit. If your policy covers $100,000 in contents, you only have $10,000 of protection while items are in transit. These policies also frequently exclude damage caused by shifting or improper packing. Most homeowners face a $1,000 or $2,500 deductible, making professional moving company insurance options a more reliable choice for smaller breakage claims.

How much does Full Value Protection usually cost?

Full Value Protection costs generally range from 1% to 2% of the total valuation you declare for your belongings. For a shipment valued at $50,000, you can expect to pay a premium between $500 and $1,000 depending on your chosen deductible. This investment ensures our certified team can provide comprehensive replacement or repair services if an accident occurs. It’s a small price to pay for the peace of mind that your entire household is secure and handled by experts.

What is a ‘High-Value Inventory’ form and do I need one?

You must complete a High-Value Inventory form for any single item valued at more than $100 per pound. This includes items like a $3,000 designer watch, a $5,000 original painting, or high-end electronics. If you fail to list these specific items, the mover’s liability is legally limited to the standard valuation level. Our professional coordinators provide these forms 14 days before your move to ensure every expensive asset is documented and protected properly.

Can I buy moving insurance if I pack the boxes myself?

You can obtain valuation for your move, but movers aren’t liable for internal breakage in boxes you packed yourself unless the exterior shows clear damage. Statistics show that 85% of damage claims involve boxes packed by owners rather than professionals. For full coverage, we recommend our professional packing services. Our skilled crew uses certified materials to ensure your items arrive safely, which qualifies your belongings for the highest level of protection available under your chosen plan.

How long do I have to file a claim for damaged items after my move?

For interstate moves, federal regulations grant you 9 months from the delivery date to file a formal written claim. However, Florida intrastate moves often follow different timelines specified in your individual service contract. We recommend inspecting all items within 48 hours of delivery and reporting issues immediately. Filing your claim within 15 days of the move date ensures the most efficient resolution and helps our team address your concerns while details are fresh.

What is the ’60 cents per pound’ rule in simple terms?

The 60 cents per pound rule is the most basic liability level, known as Released Value Protection, and it pays you based on weight rather than actual value. If a 100-pound antique dresser worth $2,000 is destroyed, the moving company only owes you $60.00. This is the default option if you don’t select Full Value Protection. It’s an economical choice for some, but it provides very little financial security for modern electronics or high-end furniture.